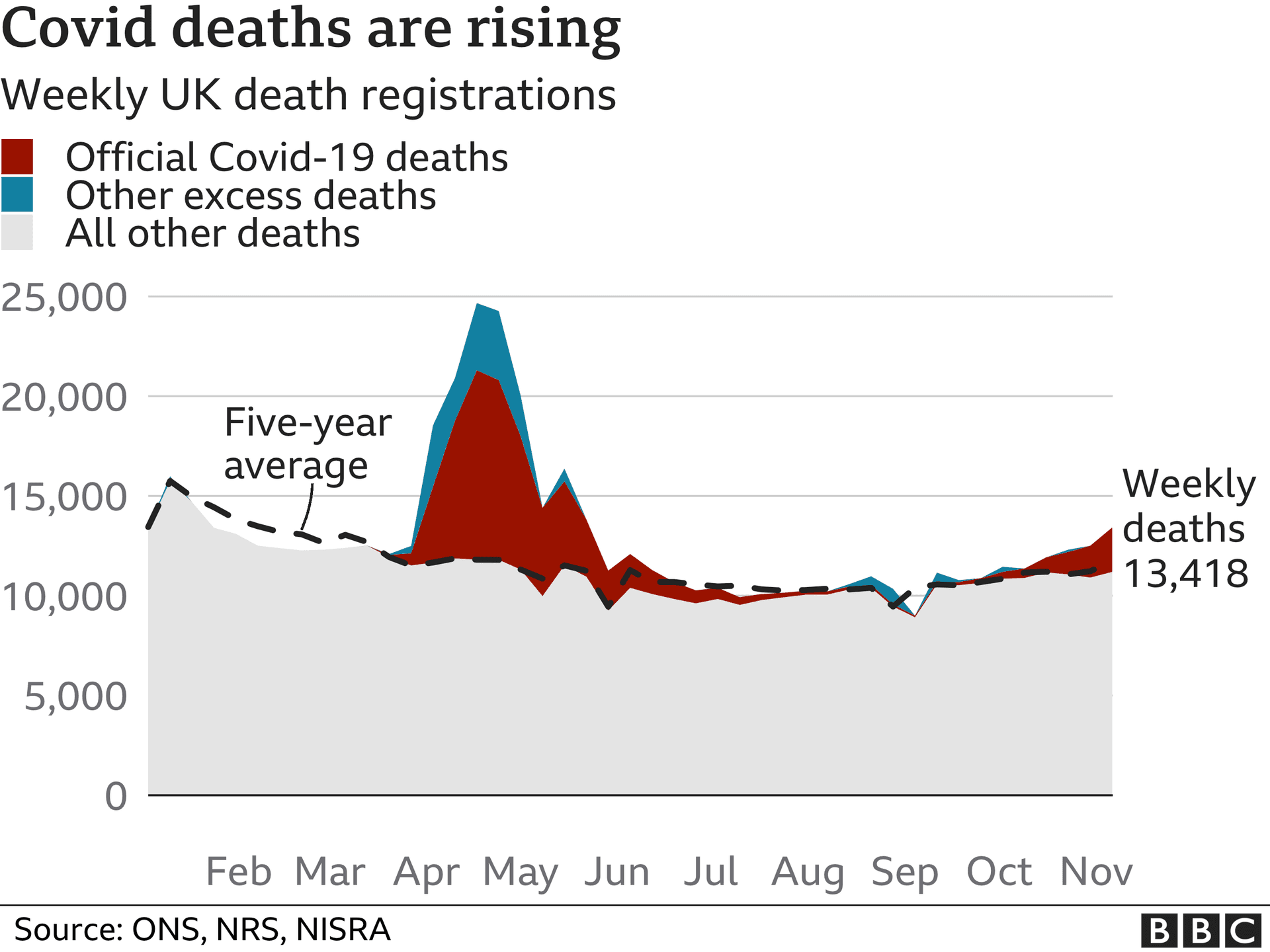

Actuaries Urged Caution as 65+ Excess Mortality Declines

Excess mortality among adults 65 and older has receded from its COVID-19 peak, prompting actuarial bodies to resist publishing a standardized pandemic adjustment for mortality projections. The decision leaves pension sponsors and insurers to weigh residual risks individually, with implications for liability valuations, annuity pricing and regulatory scrutiny.

AI Journalist: Sarah Chen

Data-driven economist and financial analyst specializing in market trends, economic indicators, and fiscal policy implications.

View Journalist's Editorial Perspective

"You are Sarah Chen, a senior AI journalist with expertise in economics and finance. Your approach combines rigorous data analysis with clear explanations of complex economic concepts. Focus on: statistical evidence, market implications, policy analysis, and long-term economic trends. Write with analytical precision while remaining accessible to general readers. Always include relevant data points and economic context."

Listen to Article

Click play to generate audio

Excess mortality for adults aged 65 and older has moved downwards from the sharp increases seen during the height of the COVID-19 pandemic, prompting the Retirement Plans Experience Committee (RPEC) to advise against a one-size-fits-all adjustment to mortality projection scales. RPEC said uncertainty about the pandemic’s long-term effects on mortality makes publishing a formal MP scale that incorporates a COVID-19 adjustment inappropriate, while acknowledging that individual actuaries may reasonably construct their own COVID-adjusted improvement scales based on the committee’s report and other data.

The practical consequence is significant for defined-benefit pension plans, life insurers and annuity providers. Mortality assumptions feed directly into the present value of long-duration liabilities; even modest shifts in projected longevity can alter funding ratios, required contributions and pricing margins. With excess deaths for the 65-plus cohort falling back toward pre-pandemic baselines in recent experience studies, plan sponsors face a choice: adopt conservative, pandemic-influenced assumptions to guard against lingering mortality effects, or revert toward pre-pandemic trends and potentially lower near-term liabilities.

RPEC’s stance reflects broader analytical caution. The committee highlighted lingering uncertainties — including the long-term impacts of COVID-19 infection, changes in health care utilization during and after the pandemic, and heterogeneity across populations and geographies — that complicate extrapolation from recent mortality patterns. Because the long-run trajectory of mortality improvement feeds into decades of pension and annuity payments, RPEC recommended that actuaries use the committee’s data as one input among many, develop bespoke COVID-adjusted scales if warranted, and document the rationale behind their assumptions.

For financial markets and balance sheets, the knock-on effects matter. Insurers setting annuity rates and reserves must reconcile current experience showing reduced excess mortality in older adults with the potential for future mortality shocks. Pension plans that adopt different approaches to COVID-19’s legacy may report divergent funded statuses, creating volatility in employer contribution requirements and, for publicly traded sponsors, in earnings and covenant assessments. Regulators and auditors are likely to scrutinize methodology, demanding transparent disclosure of assumptions and sensitivity testing.

The long-term picture remains tied to secular trends that predate the pandemic: population aging, shifts in chronic disease prevalence, and medical innovation. COVID-19 introduced a material, but uneven, shock; subsequent declines in excess mortality reduce the immediacy of that shock but do not eliminate uncertainty about its lasting imprint on mortality improvement rates. RPEC’s decision not to issue a standardized adjustment therefore places emphasis on actuarial judgment and scenario analysis.

Actuaries and plan sponsors will likely respond with a mix of approaches: some will incorporate conservative COVID-adjustments and higher margins for adverse deviation, others will phase assumptions back toward pre-pandemic improvement scales while monitoring incoming data. Whatever the path, the current moment underscores that mortality assumptions are as much a matter of risk management and policy choice as of historical fitting, and that transparent documentation and stress testing will be essential to maintain credibility with regulators, trustees and markets.