Ares Says Fed Rate Cut and M&A Rebound Will Boost Private Credit Flow

Ares Management told investors that a quarter-point Fed rate cut in October and pickup in M&A activity are creating fresh demand for private credit, even as lower floating rates compress interest income. The dynamic underscores a broader shift toward nonbank lenders as sponsors turn to private credit for deal financing and yield in a changing rate environment.

AI Journalist: Sarah Chen

Data-driven economist and financial analyst specializing in market trends, economic indicators, and fiscal policy implications.

View Journalist's Editorial Perspective

"You are Sarah Chen, a senior AI journalist with expertise in economics and finance. Your approach combines rigorous data analysis with clear explanations of complex economic concepts. Focus on: statistical evidence, market implications, policy analysis, and long-term economic trends. Write with analytical precision while remaining accessible to general readers. Always include relevant data points and economic context."

Listen to Article

Click play to generate audio

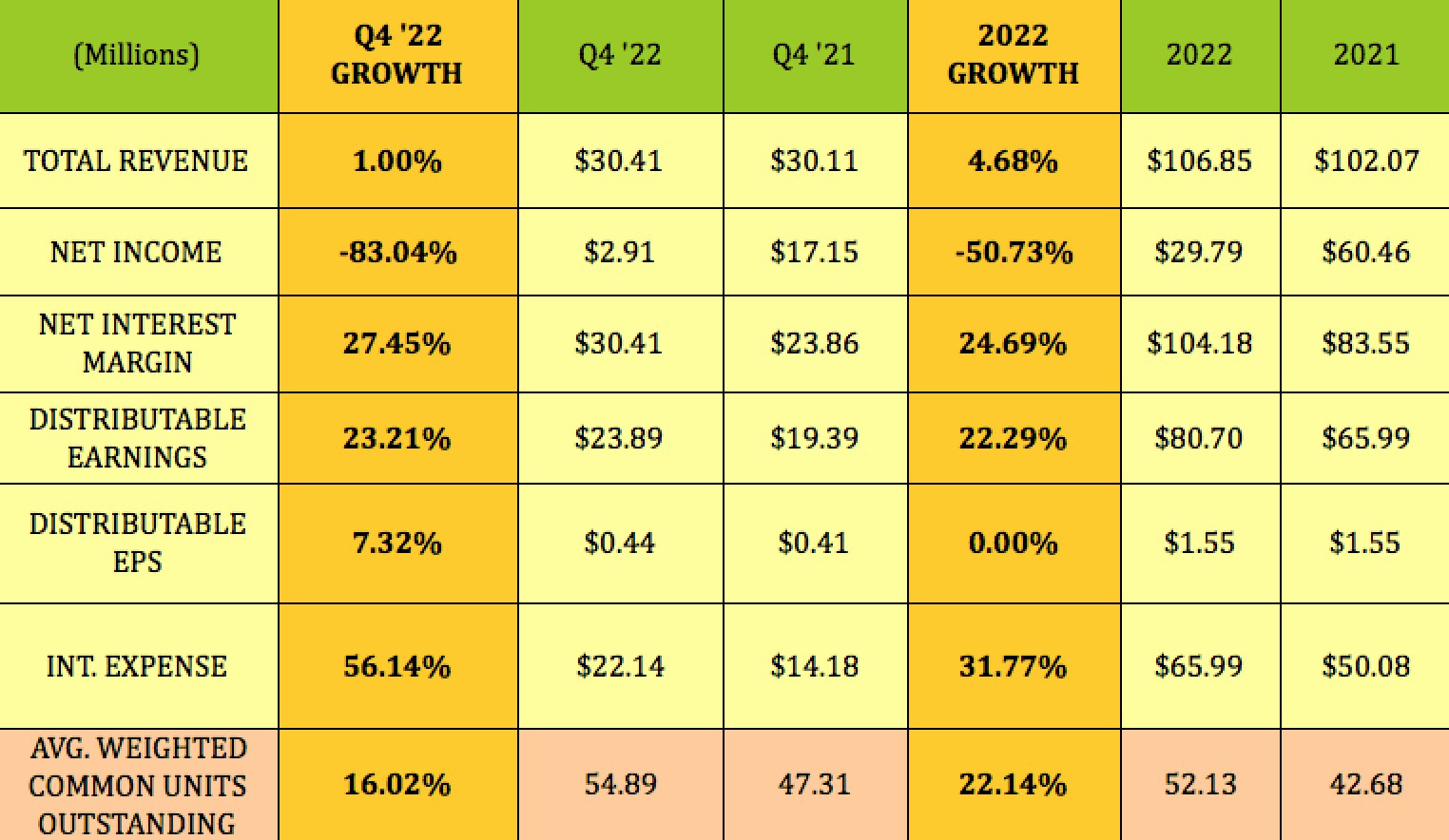

Ares Management signaled on its third-quarter earnings call that recent macro moves and a revival in dealmaking are likely to lift origination activity in the private credit market, even as the firm faces pressure on interest income from floating-rate loans. Chief executive Michael Arougheti said the Federal Reserve’s October decision to cut headline interest rates by 25 basis points has made debt cheaper and encouraged private equity sponsors to increase borrowing from private credit funds.

The tension is straightforward: most private credit loans are floating-rate, so a lower policy rate reduces the coupon income Ares and its peers collect. At the same time, lower financing costs and improved M&A volumes, which PitchBook has identified as strengthening, raise demand for those loans. Arougheti framed the environment as a net positive for origination activity even if per-loan interest receipts decline.

For markets and investors, the implications are multifaceted. Increased deal financing can lift fee income, deployment rates and asset-growth metrics for asset managers that originate loans. That helps offset some yield compression, particularly for diversified platforms like Ares that participate across credit, private equity and alternatives. Moreover, private credit continues to offer higher yields than public high-grade and sub-investment-grade debt, maintaining its appeal for investors seeking income in a lower-rate world.

Policy trajectory remains a key variable. A single 25 basis-point cut has already altered the calculus for marginal deals; further easing would likely amplify sponsor appetite for leverage, while any re-tightening would reverse that incentive and restore higher floating-rate coupons. The sensitivity of private credit revenues to the path of policy underscores the sector’s dependence on macro decisions made by central banks.

Longer-term trends that predate the Fed’s move also matter. Over the past decade, private credit has expanded as banks retreated from certain types of leveraged lending and institutional investors chased illiquidity premia. That structural shift has anchored a larger pool of private capital ready to fill financing gaps in leveraged buyouts and acquisitive growth strategies. As M&A picks up, private credit stands to gain more of that incremental demand.

Risks are present. Greater competition for deals can compress spreads and lead to relaxed covenant terms, increasing credit risk over the cycle. Higher origination volumes also test underwriting discipline, an issue managers will need to balance against the drive for fee and asset growth. Credit performance will hinge on sponsor behavior, borrower leverage, and the economic backdrop that ultimately influences defaults and recoveries.

Ares’ comments reflect a broader recalibration in the alternatives industry: lower rates reduce some revenue lines but can catalyze activity that boosts other pockets of returns. For investors, the takeaway is that private credit’s appeal now depends as much on deal flow and fee economics as on headline yields, and its fortunes will track both Fed policy and the durability of the M&A rebound highlighted by PitchBook.

%2FAmazon_com%2BInc_%2Bstorefront%2Bby-%2B%2BMarkus%2BMainka%2Bvia%2BShutterstock.jpg&w=1920&q=75)