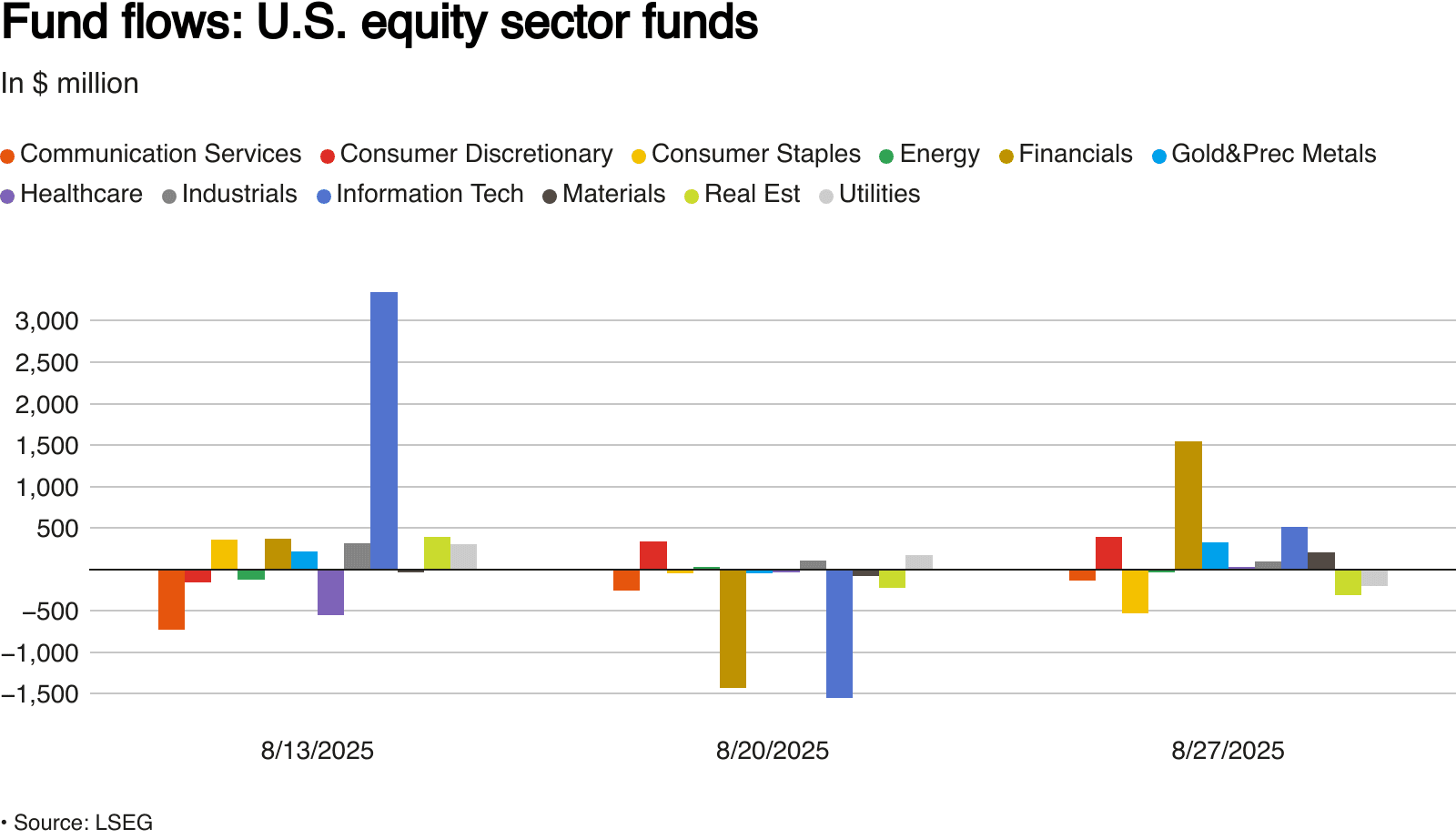

Investors Flood Money Market Funds, Seeking Shelter Ahead of Fed

U.S. money market funds have drawn billions in the week ending Dec. 9, 2025, as investors pull back from equities and long duration bonds ahead of the Federal Reserve’s policy meeting. The surge in cash is weighing on short term yields and tightening liquidity in the commercial paper and Treasury bill markets, complicating the Fed’s messaging on when easing may begin.

U.S. investors moved decisively into money market funds this week, reallocating substantial assets from equities and longer duration bonds into cash management vehicles as the Federal Reserve prepares to deliver policy guidance later in the week. Fund managers reported heavy redemptions from risk assets and heightened inflows to cash funds in the week ending Dec. 9, 2025, a clear sign of a defensive shift among institutional and retail investors alike.

Portfolio managers said uncertainty about how and when the Fed will begin cutting rates next year is the central concern. Market participants have been parsing every Fed comment for clues about the timing of easing in 2026, and this week’s rotation reflects a desire to preserve liquidity while waiting for clarity. Analysts described the flows as a tactical move to shorten portfolio duration and keep powder dry in the event of renewed volatility.

The rush into money market funds is producing concrete market effects. Increased demand for cash instruments has suppressed yields on short term Treasury bills and commercial paper in recent sessions, and dealers reported tighter conditions for placing new issuance. That dynamic is altering the normal plumbing of short term funding, as corporate borrowers and financial institutions face a more competitive environment to roll over commercial paper and issue bill paper.

The rise in cash allocations also matters for broader market liquidity. Money market funds are a major buyer of Treasury bills and repos. When inflows surge, those funds can soak up paper and drive yields lower, but the flows also concentrate liquidity into a narrow market segment. Treasury dealers warned that while bill yields have declined, secondary market depth can contract, making it harder for large issuers to execute size without moving prices.

For the Fed, these developments present a subtle policy conundrum. Officials must weigh data on inflation and labor markets against financial conditions that are in part shaped by investor expectations of future policy. Heavy cash flows signal caution about growth prospects in 2026, even as lower short term yields could ease financial conditions and indirectly support economic activity. The net effect complicates forecasting the transmission of policy changes.

The pattern also ties into longer term trends that have reshaped cash management since the sharp rate hikes of 2022 and 2023. Higher overnight and short term yields revived demand for money market funds and related products, rebuilding a sizable cash cushion across institutional and retail investors. Regulatory changes and structural shifts in banking balance sheets have also influenced where corporations park short term liquidity, increasing reliance on nonbank cash vehicles.

As Fed officials take the podium later this week, market watchers expect careful language on the pace and sequencing of cuts rather than an immediate move. In the near term, the continued inflows into money market funds will remain a barometer of investor confidence, with implications for short term yields, corporate funding costs, and the transmission of monetary policy into the broader economy.

%2Fcloudfront-us-east-2.images.arcpublishing.com%2Freuters%2FH7UAM7SDIZONBHJOIIBY6T4DZM.jpg&w=1920&q=75)