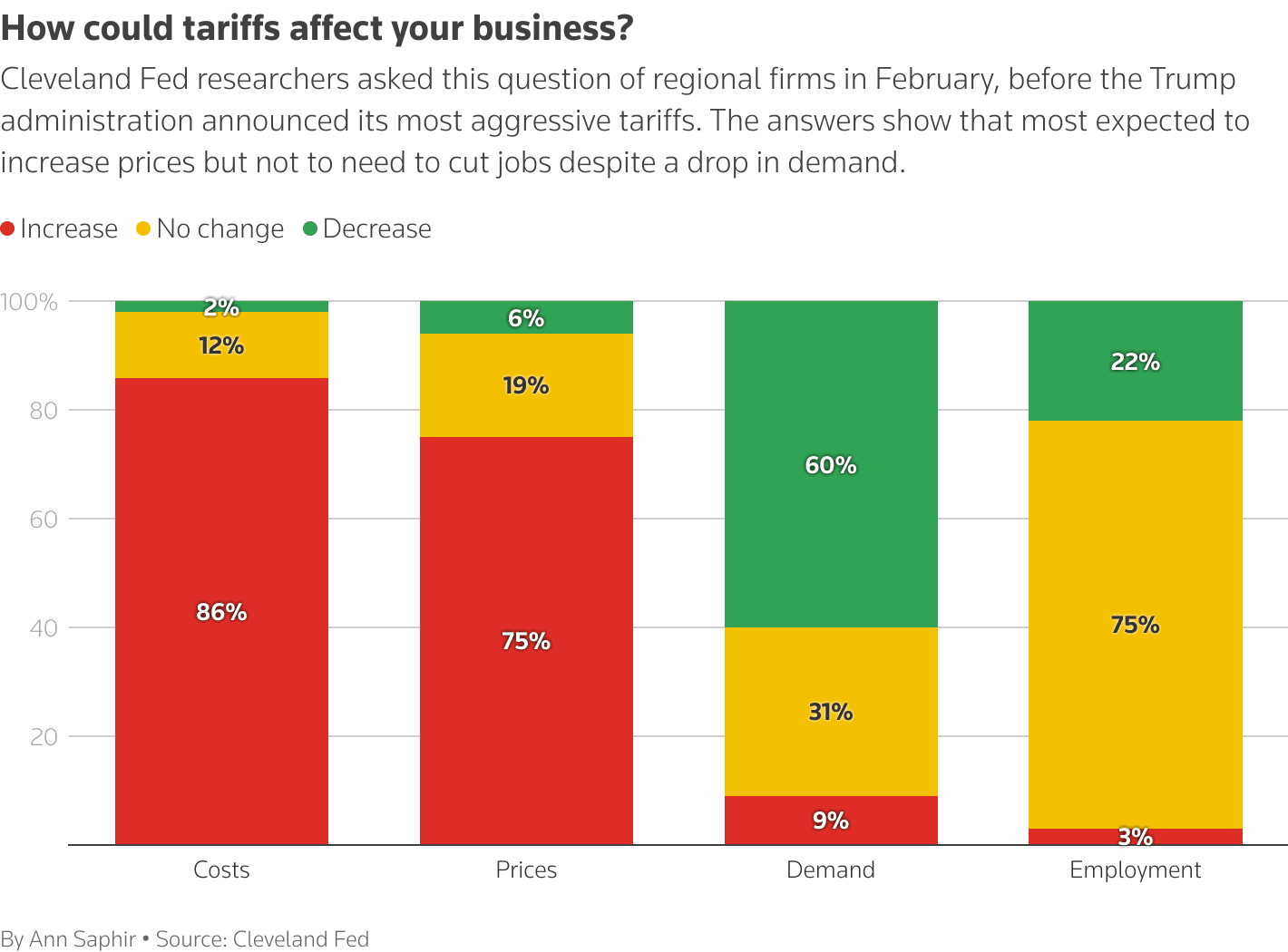

Study Finds Tariffs Lower Inflation, But Weaken Jobs and Growth

A San Francisco Federal Reserve working paper analyzing 150 years of tariff episodes in the United States and abroad finds that tariffs often reduce inflation by suppressing economic activity and asset prices, rather than by raising consumer costs. The findings complicate political claims that tariffs are innocuous for inflation, and they underscore trade offs for policymakers balancing price stability and employment.

Listen to Article

Click play to generate audio

A new working paper from researchers at the San Francisco Federal Reserve challenges the common assumption that tariffs automatically push up consumer inflation. Drawing on 150 years of tariff episodes in the United States and other countries, San Francisco Fed economists Régis Barnichon and Aayush Singh show that higher tariffs frequently produce a short term decline in inflation, accompanied by weaker economic activity and higher unemployment.

The paper describes two channels through which tariffs can cool inflation. One channel runs through real activity. By disrupting supply chains and trade volumes, tariffs reduce output and employment, lowering demand pressures that ordinarily raise prices. The other channel operates through financial markets. Tariffs can trigger drops in asset prices, tightening household and corporate balance sheets, which in turn dampens consumption and investment and reduces inflationary pressure.

The authors rely on a long term historical approach, comparing tariff spikes across countries and episodes to identify systematic effects. That statistical scope gives the study power to separate the mechanical effect of higher import costs from broader macroeconomic disruptions that follow protectionist moves. The result is a striking conclusion for trade policy debates: tariffs are not a reliable tool for raising domestic prices, and can instead act as a brake on inflation by weakening demand.

The findings arrive amid continued political debate over the inflationary impact of recent U.S. tariffs. Administration officials have long argued that tariffs imposed during the Trump era are not the primary driver of recent price increases, even as the consumer price index has crept higher since he launched his trade war in April. The San Francisco Fed paper complicates that narrative by suggesting that the net effect of tariffs on the overall price level can be lowering inflation once the broader economic fallout is accounted for.

For financial markets and monetary policymakers the study carries practical implications. If tariffs reduce inflation by suppressing employment and output, then monetary policy faces a trade off between stabilizing prices and supporting labor markets. Central banks that focus narrowly on inflation might misread tariff induced disinflation as a policy victory while overlooking the cost in terms of higher unemployment and lower growth.

The long term perspective also matters for fiscal and trade strategy. Repeated reliance on tariffs risks persistent damage to trade relationships, investment incentives and labor market performance. While tariffs may be wielded to protect specific industries, the historical evidence presented by the San Francisco Fed cautions that the broader macroeconomic side effects can be severe.

Policymakers will need to weigh these trade offs in designing a coherent response to trade tensions. The paper suggests that to preserve both price stability and employment, governments should consider targeted measures that avoid broad scale trade disruptions, and coordinate with monetary authorities to offset any demand shortfalls resulting from protectionist shocks.