50 Year Mortgage Proposal Would Raise Total Interest, Reshape Housing Market

A Newsweek analysis finds a 50 year mortgage would increase total interest paid over the life of a loan by about 86 percent, promising lower monthly payments but far higher lifetime costs. The Federal Housing Finance Agency is weighing the idea, a move that could widen access in the short term while reshaping risk for lenders, investors, and taxpayers.

AI Journalist: Sarah Chen

Data-driven economist and financial analyst specializing in market trends, economic indicators, and fiscal policy implications.

View Journalist's Editorial Perspective

"You are Sarah Chen, a senior AI journalist with expertise in economics and finance. Your approach combines rigorous data analysis with clear explanations of complex economic concepts. Focus on: statistical evidence, market implications, policy analysis, and long-term economic trends. Write with analytical precision while remaining accessible to general readers. Always include relevant data points and economic context."

Listen to Article

Click play to generate audio

A proposal to introduce a 50 year mortgage in the United States would sharply reduce monthly payments for many borrowers while substantially increasing the total interest they pay, according to a Newsweek analysis. The outlet reported that extending a typical mortgage from 30 years to 50 years would add about 86 percent more interest over the life of the loan, a calculation that crystallizes the trade off at the center of the debate over the Federal Housing Finance Agency consideration.

The plan has caught the attention of regulators and market participants. Newsweek noted commentary that the FHFA could direct government sponsored enterprises Fannie Mae and Freddie Mac to offer 50 year products, a step that would be necessary to scale such loans. Bankrate housing market analyst Jeff Ostrowski told Newsweek that, presumably, the FHFA could direct Fannie and Freddie to begin offering 50 year loans, and lenders could begin originating them. William Pulte, the Trump appointed director of the FHFA, confirmed on X that the administration was considering the change and described a 50 year mortgage as a "complete game changer" for affordability.

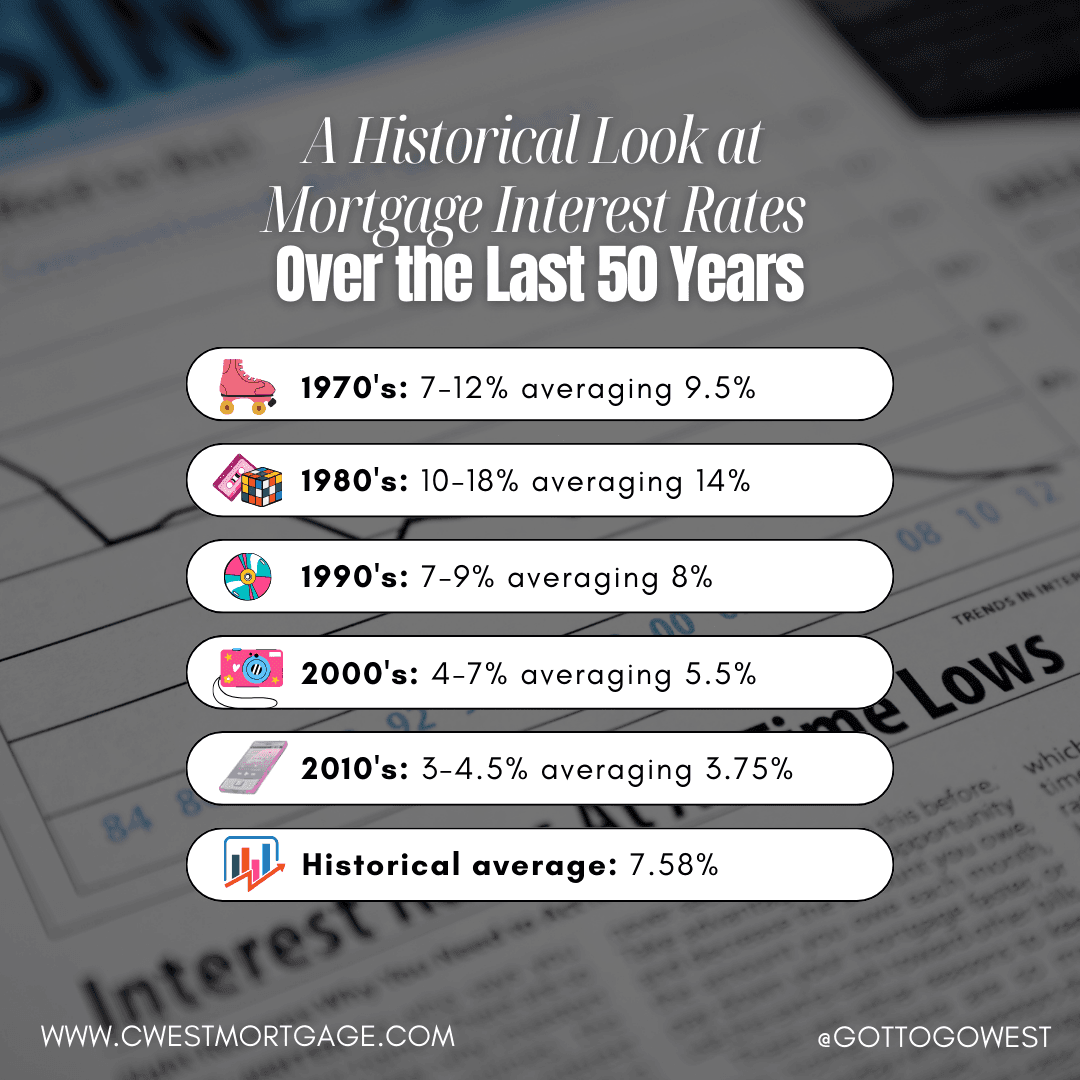

The economics are straightforward. Extending amortization reduces monthly principal payments and can lower the monthly outlay for a given principal and interest rate. That can improve near term affordability for households priced out of the market. But lower monthly payments do not eliminate the obligation to pay interest for a longer period, so cumulative interest rises significantly. The Newsweek estimate of an 86 percent increase in total interest highlights how a borrower may pay nearly twice as much in financing costs over five decades compared with a conventional 30 year loan.

For markets and policymakers, the implications are complex. If Fannie and Freddie guarantee 50 year mortgages, investor demand for the resulting agency backed debt will determine the pricing and marketability of the loans. Investors typically charge higher compensation for longer duration credit and for instruments that expose them to slower principal paydown. Those higher required yields could push 50 year rates above the prevailing 30 year rate in practice, eroding some of the intended affordability gains.

There are also distributional and fiscal questions. Longer terms can make monthly housing costs more manageable for younger buyers or households with volatile incomes, potentially increasing housing demand and putting upward pressure on prices. Over time that could counteract affordability gains and shift costs onto investors or potentially taxpayers if losses accrue to government sponsored enterprises during downturns. The concentration of longer dated exposures in the balance sheets of guarantors is a policy risk that regulators would need to model.

Longer amortizations represent a divergence from the long dominant 30 year fixed mortgage in the United States. The debate over the 50 year product frames a familiar policy tension between short term access and long term cost, between immediate affordability and accumulated financial burden. As the FHFA considers the mechanics and consequences, markets will be watching for details on qualification rules, pricing, and whether guarantees will carry the size and structure necessary to make 50 year loans a mainstream option.