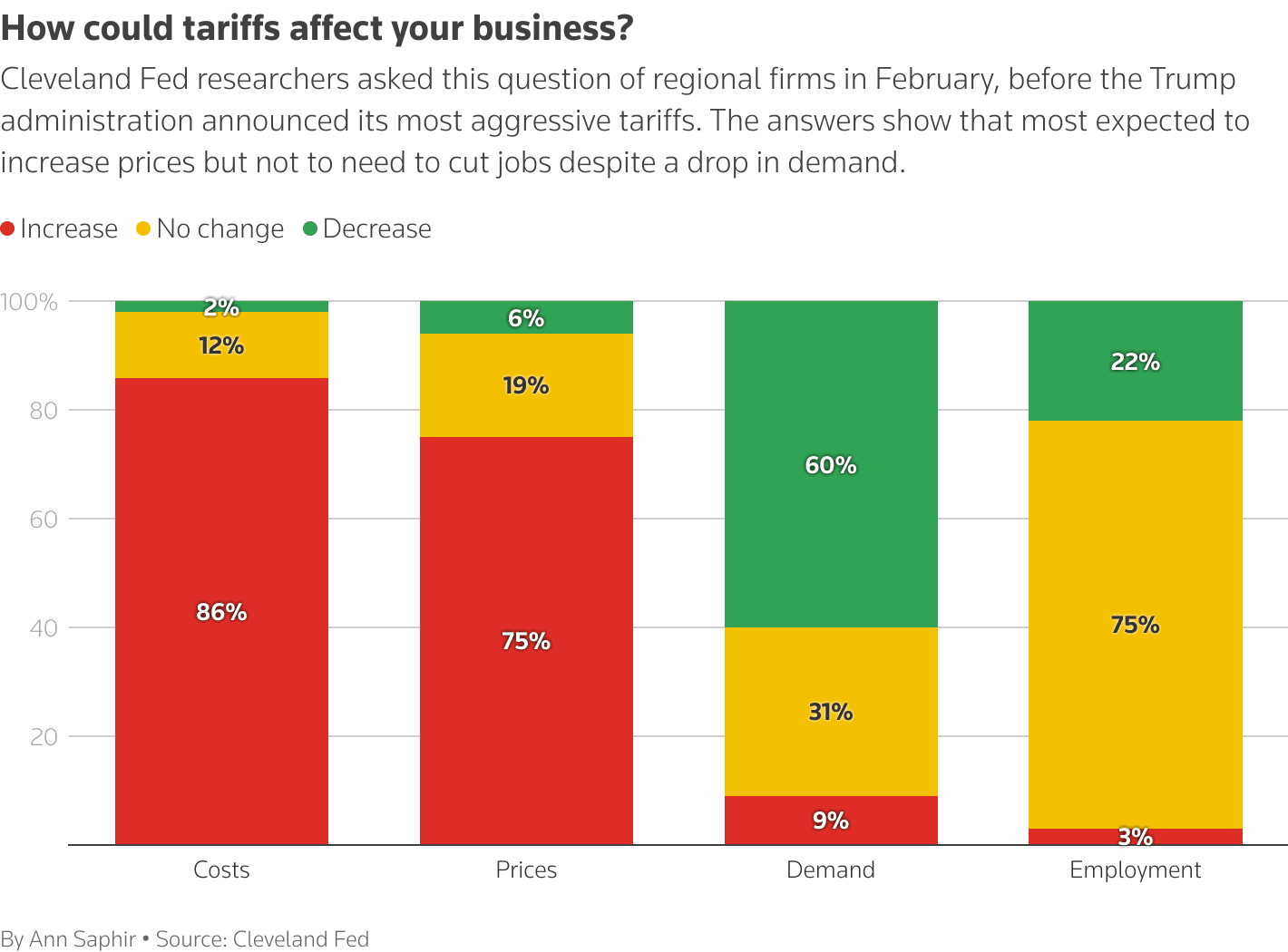

Alibaba Stock Under Pressure, AI Spending Meets Political Headwinds

Alibaba faces a fragile open as investors weigh strong growth prospects against a White House memo and a broader tech cooldown, with gaming and AI investments driving earnings forecasts. The market will watch analyst revisions and sector momentum, particularly Nvidia's dominant AI positioning, for signals on valuation resilience.

Alibaba Group Holdings enters the market with mixed signals as investors prepare for November 17 trading. The shares have retreated from a four year high reached after the company disclosed stepped up AI spending in late September, yet remain well above their 52 week low. Market nervousness was amplified recently when a White House memo triggered a fresh pullback, underscoring how political and regulatory developments can quickly alter sentiment for Chinese technology names.

Operationally Alibaba is leaning on a diversified growth playbook. Gaming remains a core driver, and the company has disclosed a collaboration on an x86 system on chip, a move that could deepen its footprint in game development and data center edge computing if execution meets ambition. Several research and data providers now project Alibaba’s earnings to grow in the high teens next year, with consensus EPS forecasts moving from roughly $7.9 to $9.3. Those estimates imply continued double digit profit growth, contingent on management translating AI investments into scalable revenue streams.

Analysts continue to split the difference between optimism about revenue trajectory and caution about valuation. Some models assume improving monetization at cloud and commerce businesses as AI features drive higher engagement and advertising yields. Other scenarios emphasize execution risk, potential regulatory friction, and macro sensitivity if global rate expectations shift.

The broader context for Alibaba includes a tech sector narrative shaped by Nvidia and the AI hardware cycle. Oppenheimer analyst Rick Schafer recently raised his EPS forecasts for 2025 through 2027 to $4.56, $6.93, and $8.50 respectively, reiterated an Outperform view, and lifted a price target on Nvidia to $265. Schafer expects data center revenue at Nvidia to surge about 58 percent year over year and 19 percent quarter over quarter as customers migrate to new GB300 chips. That report highlighted a backlog of roughly 20 million GPUs and shipments already at about 6 million, while interconnect products such as NVLink, Spectrum X, and Infiniband are expected to bolster networking revenue. Nvidia’s dominant position in AI hardware is underpinning a premium multiple for the company and shaping investor expectations across the cloud and data center ecosystem.

For Alibaba, the immediate risk calculus is twofold. First, political developments such as the White House memo can induce short term volatility and complicate cross border flows into Chinese tech stocks. Second, global sentiment toward tech valuations is sensitive to interest rate direction, with markets also parsing the likelihood of a December policy easing which could support higher multiples. On the constructive side, analysts’ upward EPS revisions and the gaming SoC collaboration offer a tangible operational narrative for growth beyond commerce.

Investors will be watching upcoming quarterly guidance, cloud adoption metrics, and any further regulatory signals. Long term the question is whether Alibaba’s AI and gaming investments can sustain high teens earnings growth while navigating geopolitical and macroeconomic cross currents that continue to shape market access and valuation.