China factory activity shrinks again, services cool into crucial policy window

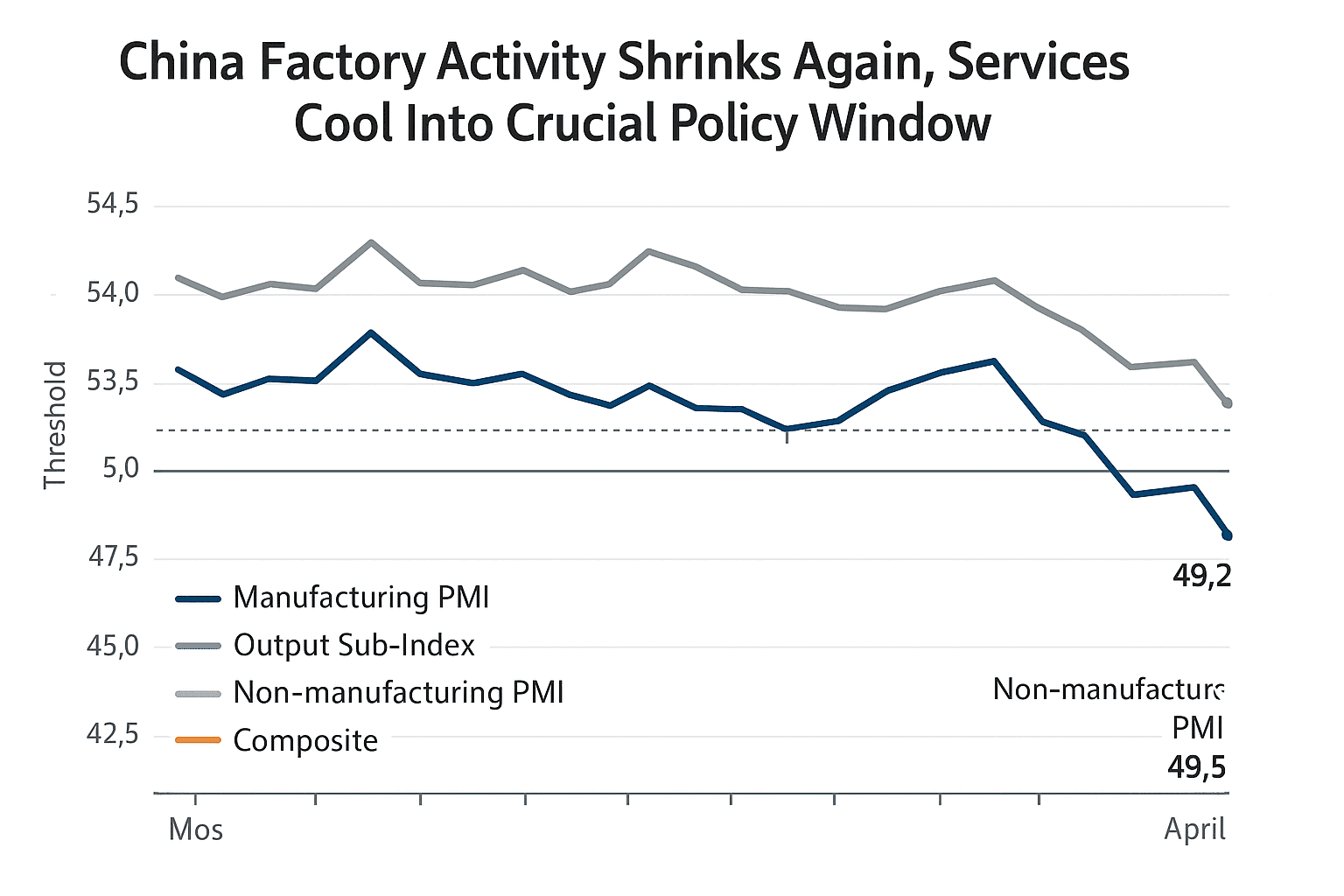

China’s factory sector contracted for an eighth straight month in November while service sector activity slipped below growth territory, intensifying a debate in Beijing over whether to deepen structural reform or deploy broader stimulus. With manufacturing PMI at 49.2 and the non manufacturing gauge at 49.5, the readings point to soft domestic demand that could shape policy choices into early 2026.

China’s manufacturing sector continued to struggle in November, extending a run of contraction to eight months, as a separate measure showed services cooling to levels last seen more than a year ago. The National Bureau of Statistics reported a manufacturing purchasing managers index reading of 49.2 for November, up slightly from 49.0 in October but still below the 50 threshold that separates expansion from contraction. The bureau said the output sub index stood at 50.0, indicating production largely stalled, while new orders and new export orders ticked up from October yet remained below the growth cutoff.

The non manufacturing PMI, which covers services and construction, fell to 49.5 from 50.1 in October, marking the first contraction in the sector since December 2022. The composite PMI for manufacturing and non manufacturing dropped to 49.7 from 50.0 in October, putting overall business activity inching below the growth line. Services activity slid below 50 for the first time since September 2024, with particularly weak readings in real estate related services and household services, a reflection of continuing strain in property markets and weak consumer spending on big ticket and discretionary items. At the same time a services business outlook sub index registered 55.9, suggesting firms retain some confidence in future demand even as current activity softens.

The data underscore the dilemma facing policymakers as China approaches the end of its 2025 policy horizon. Officials have pointed to targeted measures to boost consumption, but economists cited in market commentary expect any large scale stimulus to be postponed until early 2026 given the government’s 2025 growth target of around 5 percent. The combination of a protracted property downturn, heavy local government debt burdens and softer external demand has constrained the scope for rapid fiscal or monetary loosening.

Market implications are immediate. Weak manufacturing and services readings typically weigh on equities tied to industrial activity and commodities exporters, while prompting investors to reassess the trajectory for interest rates and credit support. For Beijing the choice is stark. Leaning into stimulus risks slowing progress on structural reforms that officials have made central to long term economic resilience. Holding the line on reform could prolong a soft patch in domestic demand and delay a sustained recovery.

Long term trends complicate the picture. A persistent property adjustment, an aging population and a pivot toward higher value services and technology driven growth require policy measures that balance demand support with supply side improvement. The upbeat services outlook sub index offers a potential foothold for recovery if consumption measures succeed in restoring confidence. For now November’s PMI print signals that China’s tentative rebound remains fragile, and that policymakers will face continued pressure to calibrate actions carefully as they weigh short term stabilization against longer term transformation.