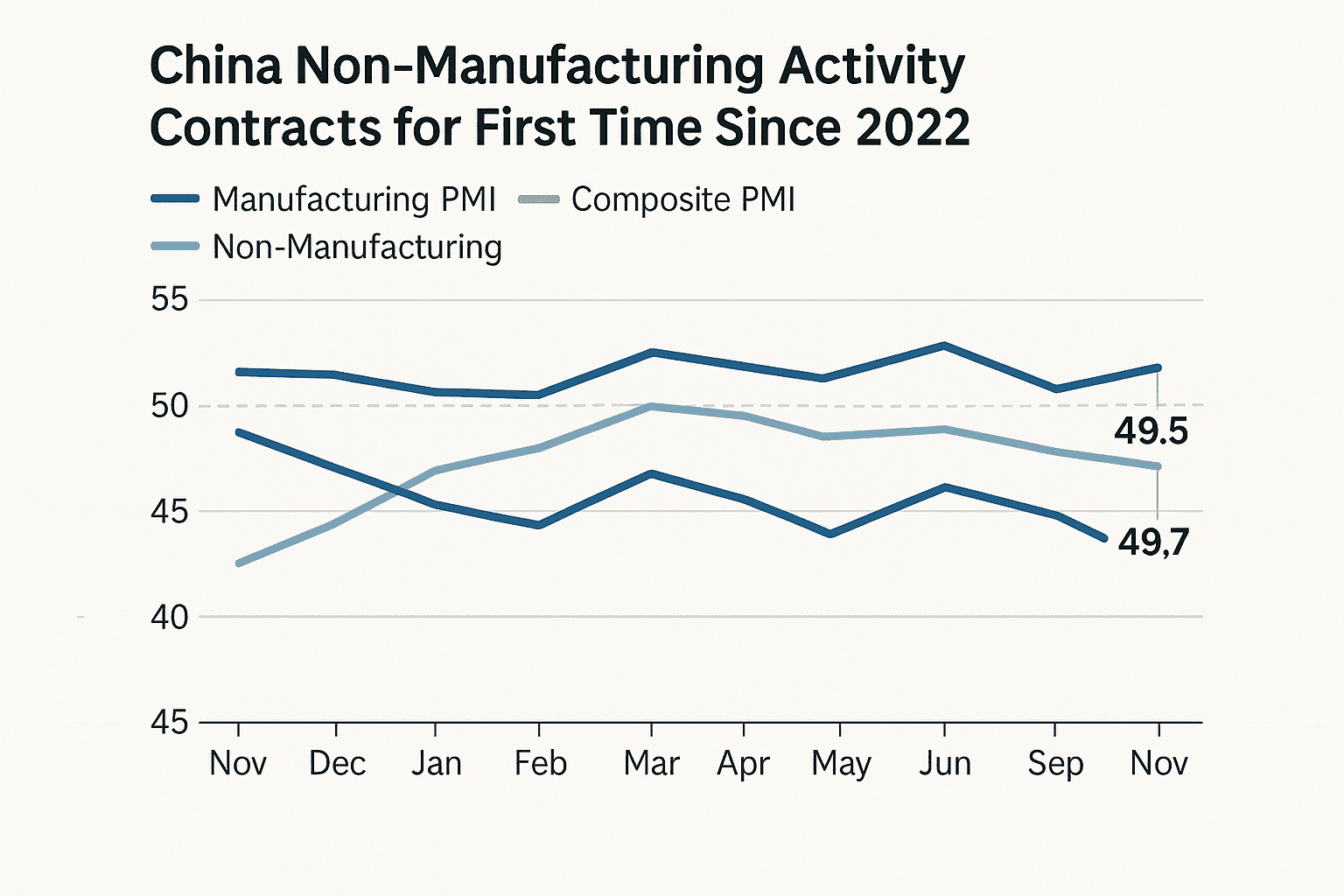

China non manufacturing activity contracts for first time since 2022, composite PMI slips below 50

An official survey released November 30 2025 showed China’s non manufacturing sector contracted in November for the first time since December 2022, with the non manufacturing PMI falling to 49.5 from 50.1 in October. The composite PMI dropped to 49.7, signalling broader weakness and adding pressure on Beijing to consider further stimulus as global demand and export headwinds persist.

China’s non manufacturing sector, which covers services and construction, contracted in November for the first time since December 2022 according to an official survey released on November 30 2025. The non manufacturing PMI fell to 49.5 from 50.1 in October, while the composite PMI, which combines manufacturing and non manufacturing activity, slipped below the 50 expansion threshold to 49.7. The deterioration underscores a widening slowdown after months of weak factory output.

The official manufacturing PMI has been in contraction for eight consecutive months, reinforcing a pattern of subdued industrial activity that has been apparent across multiple indicators this year. Together the readings point to a broad softening in both external facing sectors and those driven by domestic consumption. Services, which account for a growing share of economic output and employment, are particularly sensitive to household spending. A contraction in non manufacturing activity therefore heightens the risk that domestic demand is failing to pick up, complicating Beijing’s efforts to rebalance growth away from heavy industry and toward consumption.

Analysts and officials have warned that if domestic demand does not stabilise, fresh policy support will be necessary. The latest PMI data increases the urgency for such measures by signalling that weakness is no longer confined to factories. Chinese policymakers face a trade off between providing enough stimulus to shore up demand and avoiding the build up of structural imbalances. Traditional policy tools include targeted fiscal spending on infrastructure and support for local governments, credit easing for small and medium sized enterprises, and measures to lift household consumption such as tax relief or rebates. The government will also weigh the limited space left for large scale monetary easing given concerns over financial stability and debt.

The readings have immediate implications for global markets and commodity demand. Slower services activity in China typically translates into weaker consumption of energy and intermediate goods. Export facing sectors are already under pressure from soft external demand, and the combination of slowing domestic services and prolonged manufacturing weakness could reduce imports of commodities and components, affecting exporters from Australia to Brazil. Financial markets are likely to interpret the data as increasing the probability of additional policy support, a dynamic that could influence global risk sentiment and commodity price trajectories in the near term.

Longer term, the November contraction highlights the fragility of China’s economic transition. Rebalancing toward a service led, consumption driven model requires sustained household income growth and confidence. Repeated weak PMI readings in both manufacturing and non manufacturing raise questions about the pace of that transition and the potency of policy tools in addressing structural restraints such as demographic trends and high corporate leverage.

For now the data puts Beijing on notice. With the composite PMI under 50 and factory activity in persistent decline, policymakers will face renewed pressure to act if growth momentum does not recover in the coming months. The international community will be watching closely for both the substance and scale of any response, and for signs that China’s demand slowdown will ripple through global markets.