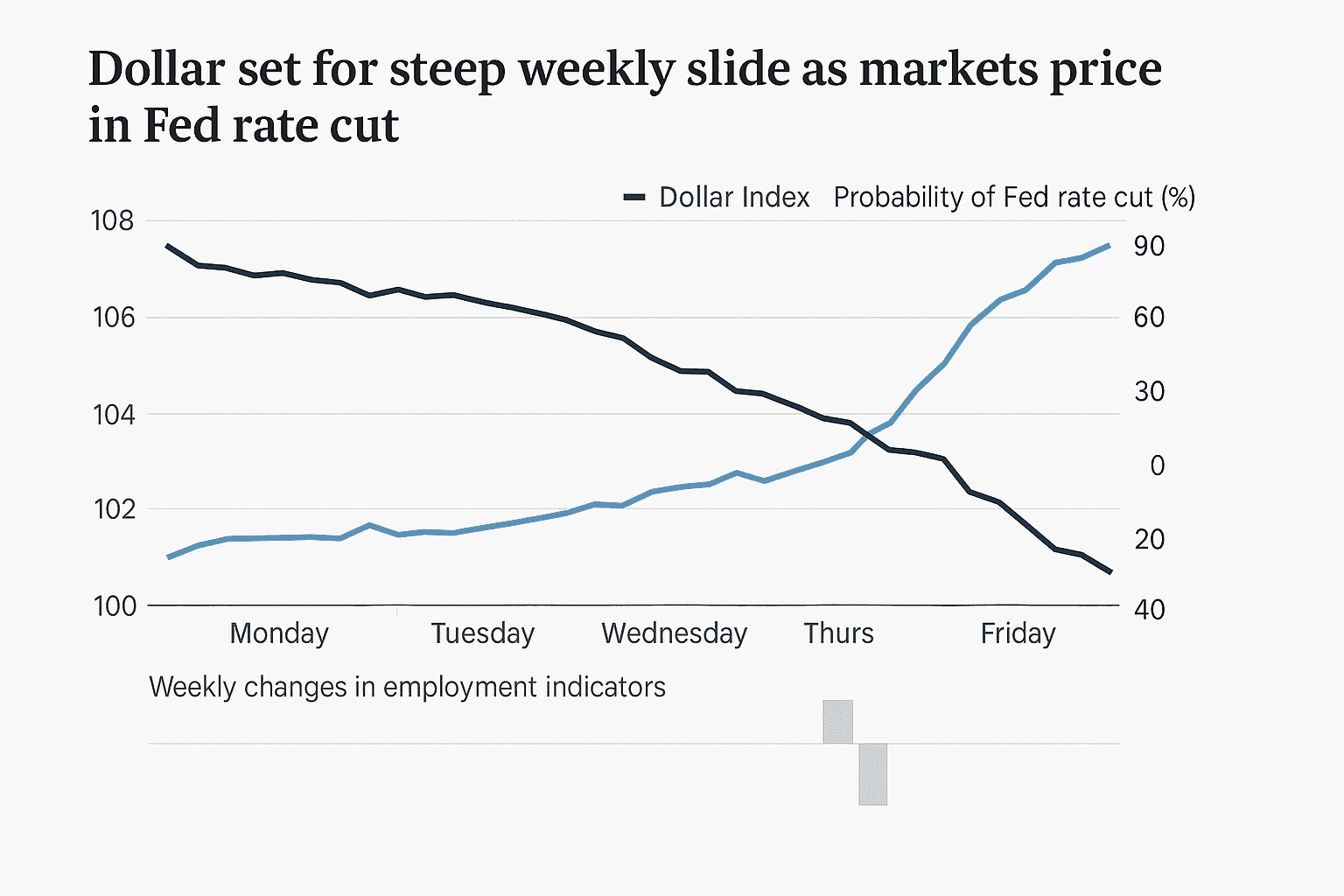

Dollar set for steep weekly slide as markets price in Fed rate cut

The U.S. dollar plunged through last week as traders sharply increased bets that the Federal Reserve will cut interest rates at its December meeting, sending the dollar index toward its largest weekly drop since late July. The shift in expectations followed weaker U.S. labor data and a string of softer economic releases after the economy reopened following a prolonged government shutdown, a dynamic that could reshape cross‑asset flows and global borrowing costs.

Currency markets digested a rapid shift in expectations last week as the U.S. dollar fell and futures traders priced in an 87 percent probability of a 25 basis point Federal Reserve rate cut at the December 9 to 10 meeting. The change reflected a string of weaker U.S. economic readings, notably on employment, and a broader reassessment of the Fed’s path as the economy reopened after a prolonged government shutdown.

The dollar index, which tracks the greenback against a basket of major currencies, was down on the week and on track for its largest weekly fall since July 21. Market participants cited softer-than-expected labor market indicators among the proximate catalysts. Those data reduced the perceived urgency for restrictive policy, prompting traders to push down short-term U.S. interest rate expectations and to reposition across currencies and risk assets.

The re-pricing was not without disruption. An outage at a CME Group data centre briefly halted trading on some platforms, interrupting price discovery in a compressed trading window before systems were restored and activity resumed. The interruption added to intraday volatility as participants adjusted book exposure to the rapidly changing Fed outlook.

The market move underscored how sensitive the dollar is to shifts in monetary policy expectations. A lower expected terminal Fed funds rate typically reduces demand for dollar funding and compresses yields on dollar-denominated assets, with knock-on effects across global markets. Investors repositioned accounts that were long the dollar or short foreign currencies, and asset managers weighed the impact on portfolio returns and hedging needs heading into year end.

For the Federal Reserve, the incoming data set presents a policy quandary. Weaker labor market prints could ease the case for further tightening, but officials will balance that against persistent inflationary pressures and the lagged effects of policy. Traders have interpreted the recent data as sufficiently soft to justify easing in December, vaulting forward rate cuts from low-probability scenarios into near-certain outcomes in market pricing.

Global implications are consequential. A softer dollar tends to relieve pressure on emerging market borrowers with dollar-denominated liabilities and can provide some upward support to commodity prices, which are typically priced in dollars. Conversely, a weaker dollar may boost U.S. inflation through higher import costs over time, complicating the Fed’s medium-term inflation outlook.

Looking ahead, the durability of the dollar’s slide depends on incoming U.S. economic releases and Fed communication between now and the December meeting. If labor conditions show renewed resilience or inflation readings surprise to the upside, markets could reverse course. If weakness persists, the dollar may continue to unwind gains from earlier in the year, prompting portfolio rebalancing across fixed income, equities and currencies as investors adjust to a lower expected interest rate environment.